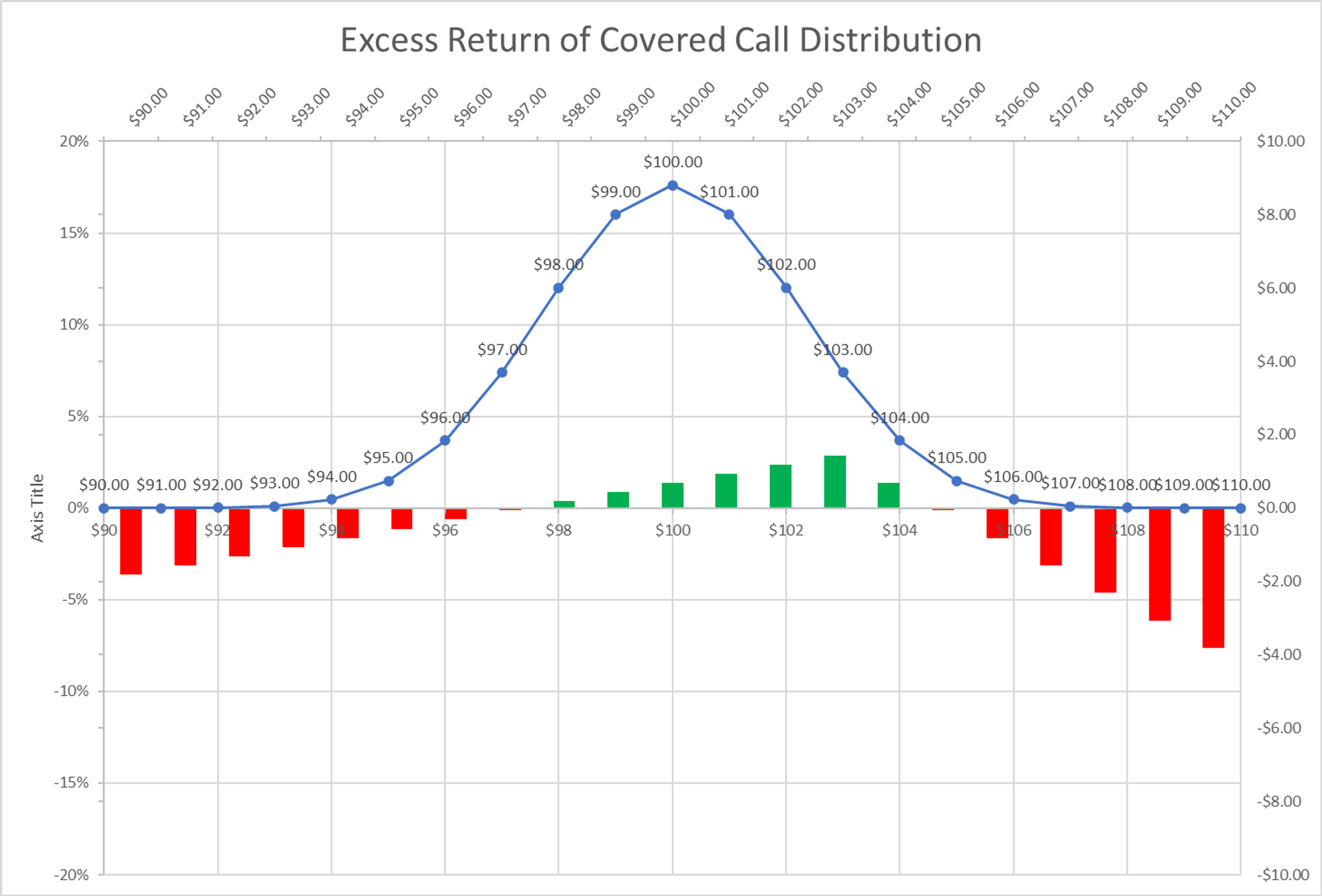

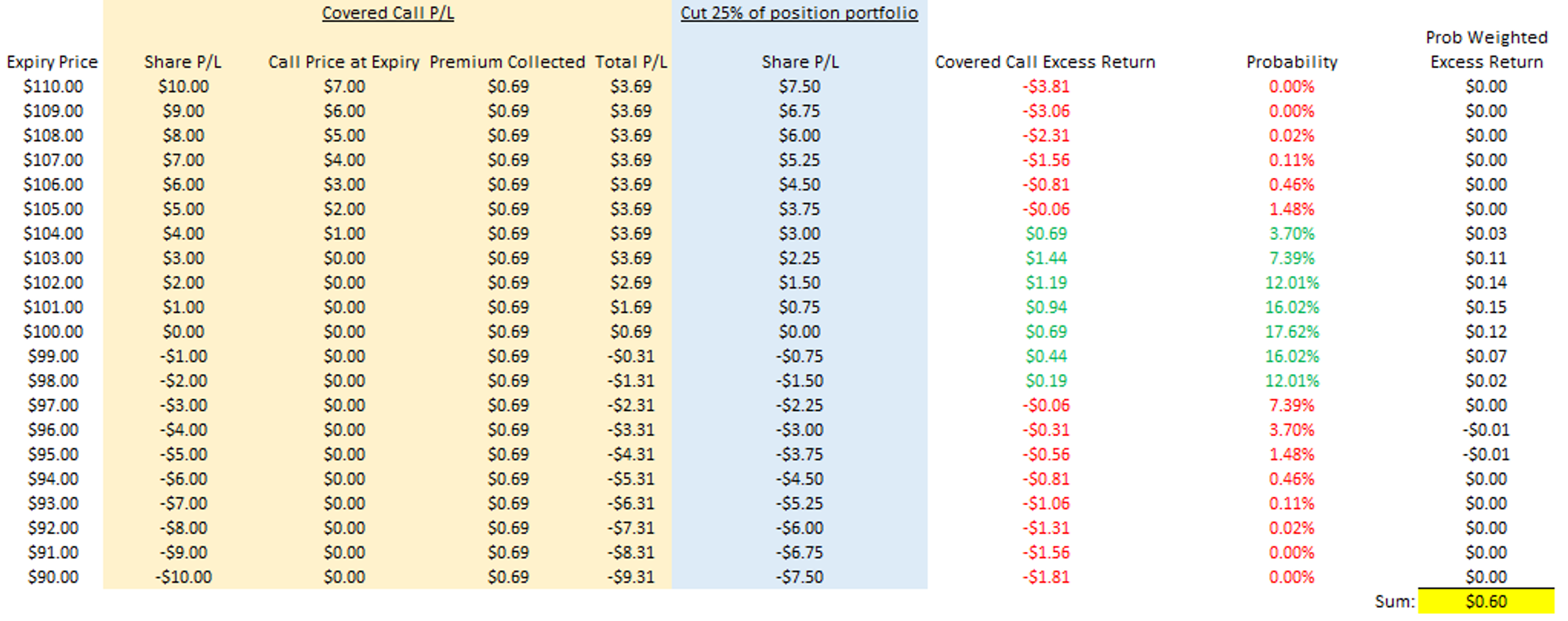

- Covered call outperforms ~85% of the time

- You sold the 103 call at $.69…you expect to make $.60 of probability-weighted excess return since the stock only moves $.50 per day instead of $1

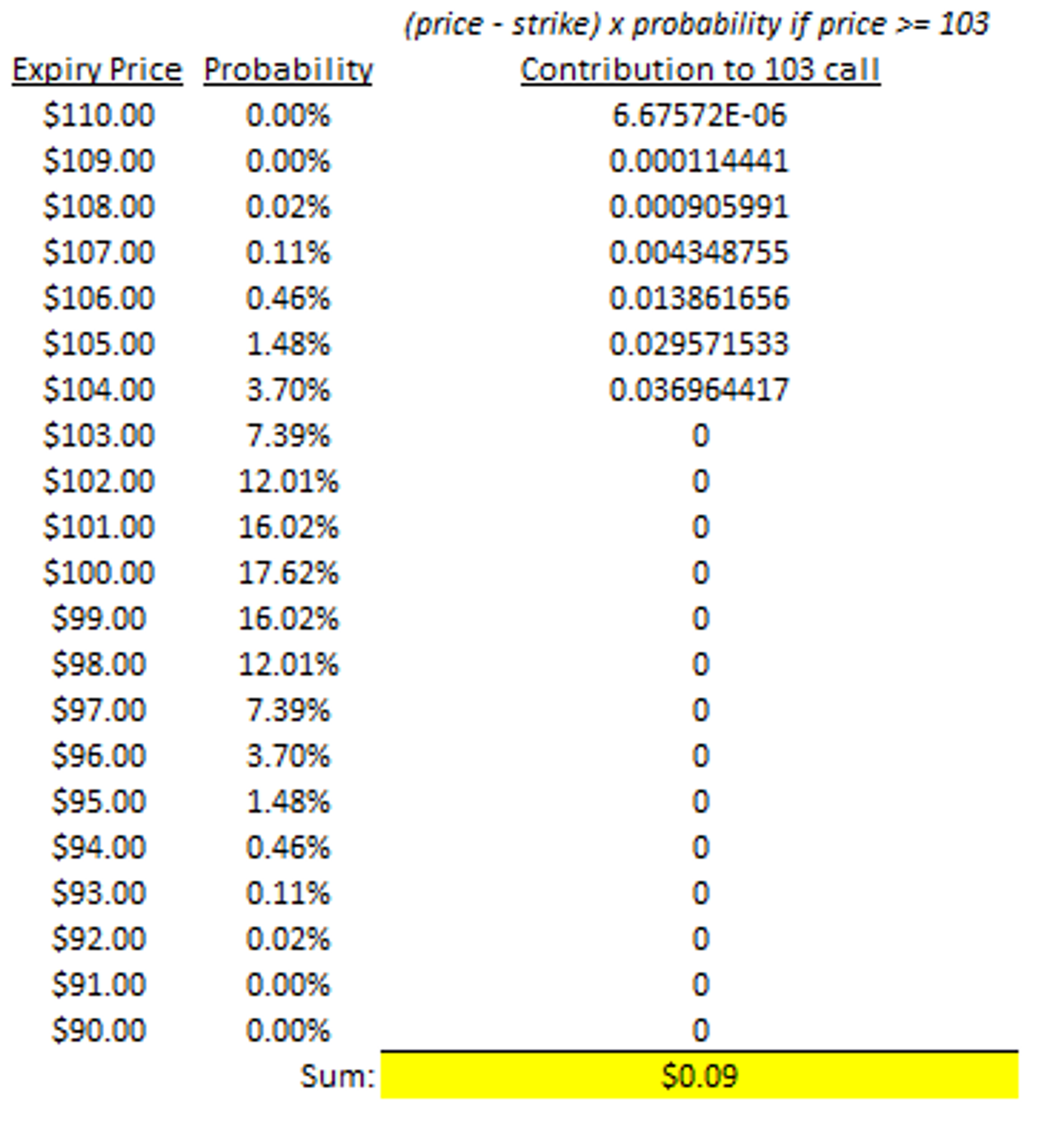

- This is confirmed by our binomial tree model where we compute option prices arithmetically. If the stock only moves $.50 per day the 103 call is worth $.09